On 8 March 2022, the European Commission proposed a series of measures for addressing the EU’s energy insecurity. The proposal was developed in response to soaring natural gas prices and broader concerns of overdependence on Russian natural gas. Proposed measures include both immediate and longer-term interventions. Crucially, diversification of supply is included as one of the key levers for addressing EU energy security for the medium and long-term. However, there is a need and an opportunity to go beyond the steps identified by the European Commission. Enhancing access to Caspian and Central Asian natural gas is the best option for EU supply diversification.

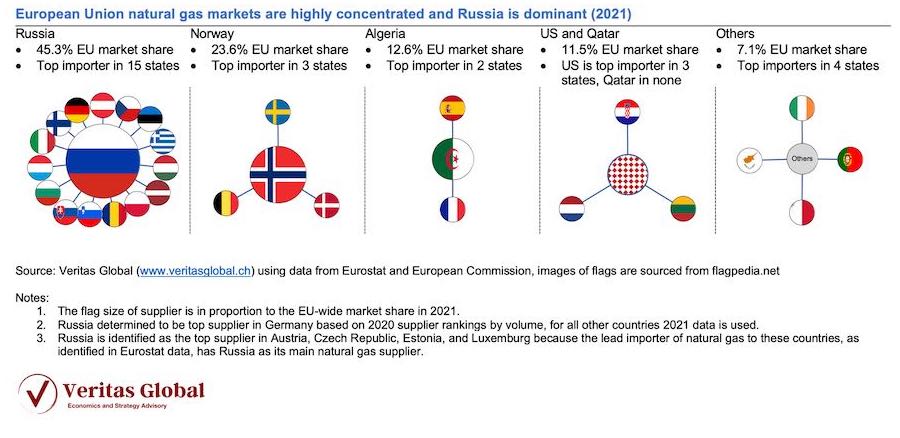

The level of market concentration and extent of Russian dominance sheds light on the scale of the challenge facing the EU. About 90% of natural gas consumption in the EU is met through imports, with about 45% of all imports coming from Russia in 2021. The other main gas suppliers to the EU were Norway (23.6%), Algeria (12.6%), the United States (6.6%) and Qatar (4.9%). For 15 of the 27 member states, Russia was the top supplier.

Diagram 1:

In the short-to-medium term, European consumers, especially in countries that are highly dependent on Russian natural gas, do not have alternative economically viable substitutes. There are limited credible options for switching at short notice to other suppliers of natural gas or to use product substitutes to natural gas. The high cost of switching to alternative options partly explains the upward price volatility observed across many EU gas markets in recent months.

The EU has prioritized development of hydrogen-based energy Aobtained by using renewable energy as one of the main responses to addressing supply side dependence in natural gas markets.

While this strategy offers an ambitious program for long-term decarbonization, it does little to address the EU’s short- and medium-term energy security needs. The EU’s hydrogen strategy, if fully implemented, targets production of up to 10 million metric tons of renewable hydrogen in the EU by 2030, which is the energy equivalent of about 5% of current natural gas demand in Europe. Even if all goes to plan, the EU hydrogen strategy implies that renewable hydrogen will not be effective at containing Russian’s dominant position in natural gas markets for at least the next two or possibly even three decades.

The scale of the structural challenges facing natural gas markets in Europe can only effectively be addressed through decisive EU action on supply diversification.

The EU’s best option to diversify supply is to tap into resources in non-Russian countries of the Caspian basin and Central Asia, which are home to about one quarter of all proven natural gas reserves globally.

The reality is that the EU has limited alternatives to Russian gas. North Sea production is at capacity and reserves have been significantly depleted, making it difficult to maintain and grow supply. Algeria is already doing its part to supply the EU, with market share of natural gas imports increasing significantly in recent years. Suppliers of liquefied natural gas (LNG) are expected to boost production, but it is uncertain whether they can be a reliable source for meeting EU demand in the medium-to-long term. Qatar can significantly boost LNG production but is better positioned to serve markets in Asia. The US may continue to supply modest quantities of LNG to Europe, but it is unlikely to become a large-scale supplier as it will be increasingly difficult for it to meet local natural gas demand while at the same time support large-scale exports.

The benefits for Europe to access the vast energy pool in the Caspian and Central Asia are partially being realized through the Southern Gas Corridor, a project that was operationalized at the end of 2020 and continues to increase deliveries. However, the scope for scale-up is far greater than what is currently planned to be implemented. One of the best options for enhancing diversification of natural gas supply to Europe is to develop additional capacity that brings Caspian gas to European markets through transit routes that do not pass through Russia or other members of the Eurasian Economic Union.

The option that offers the best supply diversification benefits (known as White Stream) would bring natural gas from the Caspian to the EU. The technical aspects of this option have been assessed in detail with feasibility studies supported through EU funding for common projects of interest. However, a lack of political will combined with misplaced concerns over climate change impacts has meant that the project has not received a green light despite being nearly shovel ready. The slow progress of developing this corridor has given Russia a dominant position across European gas markets and in practice has increased EU’s reliance on coal for electricity generation.

This article was written using the analysis of Veritas Global contained in the policy brief, Caspian Gas Is Key to EU Supply Diversification.

{kind=link}

Discussion about this post