DOW 42,187 (+30), S&P 500 5,710 (+1), Russell 2000 2,195 (-2), NYSE FANG+ 11,308 (+89), ICE Brent Crude $74.42/barrel (+$0.86), Gold $2,679/oz (-$12), Bitcoin ~60.3k (-865)

- All eyes on the BLS non-farm payrolls tomorrow

- U.S ISM Services PMI strong

- Profit-taking

- U.S. Treasury yields higher

- Oil short covering

- 3 of 11 S&P 500 Sectors higher: Energy leads, Consumer Discretionary lags

- Check out some of the recent ICE Data/Content:

- Inside the ICE House 439: Eastman CEO Mark Costa Reinvents Recycling for the Circular Economy

- Inside the ICE House: Market Storylines

- ICE September Mortgage Monitor – Rate drops make August most affordable month since February, as home price growth cools to 12-month low

MAC Desk Commentary:

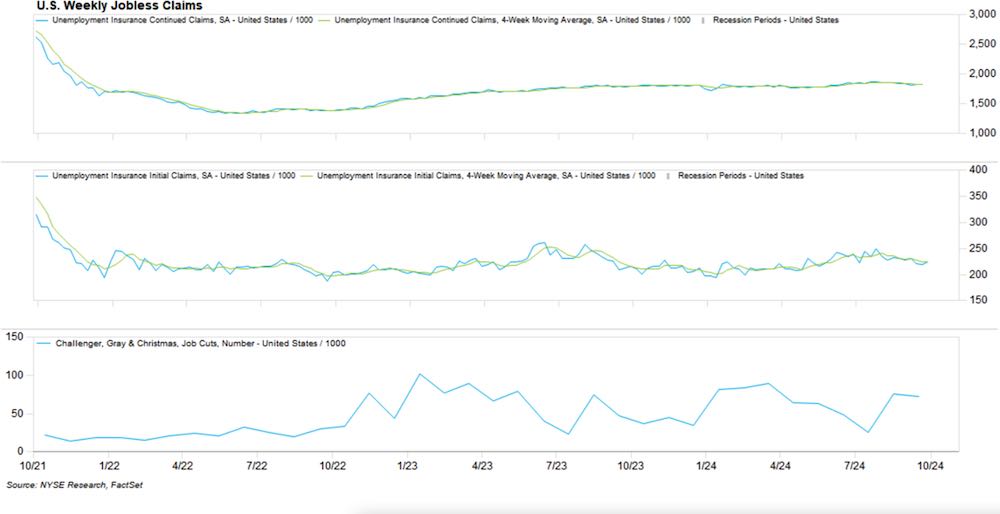

U.S equity averages finished slightly up after a soft session yesterday given rising Middle East woes. Upside came from Energy, semiconductors, and mega cap tech. The S&P 500 closed at 5709 dwindling near its 20d ma. The Russell 2k sold off as the VIX ticked higher. Today, Weekly Jobless Claims and the Challenger Job Cuts indicator were steady suggesting labor market resiliency (chart below) ahead of BLS payrolls tomorrow. The ISM Services PMI expanded more than anticipated. U.S Treasury yields pricing in modest geopolitical risk premium at this stage, 2yr at 3.69%. S&P 500 is lower within a tight range breaking below 5700 (LOD 5684). The U.S ports strike is on day three and the VIX has a 20 handle. As we head to print, the S&P 500 is up 1pts to 5,710 (+0.0%), the Dow is up 30pts to 42,187 (+0.1%), while the Russell 2k is down 2pts to 2,195 (-0.1%).

The Asian session closed lower. New PM Ishiba and BoJ Ueda had dovish remarks which coupled with stronger USD led to weaker JPY currently at 146.658. This led to a rally in the Nikkei and Topix. The final reading of Jibun Bank Services PMI confirmed expansion for a third month. China, Taiwan, and South Korea were closed. Europe finished lower. EU Services PMI (final print) increased again into expansion at 51. ECB officials are confident that inflation nearing target. Core and periphery yields higher. More downside on EUR at 1.10271 as futures point to ECB easing. GBP dipping >-1.2% and Gilt yields down as BoE Gov Bailey sees chance of more aggressive rate cuts. Germany is closed on holiday.

Weekly Jobless Claims point to a steady labor market on a seasonally adjusted basis. Non-seasonally adjusted initial claims were 1k lower. Continuing claims had a downward revision in the prior month. Initial claims were close to estimate and their 224k 4wk average. Continuing claims were flat to prior month and slightly lower than 1829k 4wk average. Challenger Job Cuts came in at 72k which is fewer cuts than prior month. It compares to 47.5k persons a year ago and it’s tracking closer to the 3mo average.

U.S data continues to come in relatively sound, introducing questions on whether Fed will implement the remaining 50bps by year-end. The ISM Services PMI was overall solid and the best since Feb 2023 though it has been historically volatile. Looking at the components, Services Employment moved below 50 giving some insight on what tomorrow’s BLS might bring. New Orders and Inventories further expanded signaling decent demand. Prices Paid rose to the highest since early 2024. New Export Orders also accelerated. The final print of the S&P Global Services PMI matched previous number showing expansion. Factory orders mixed.

As Q3 earnings start rolling in, Constellation Brands (STZ -3%) posted mixed earnings and mgmt. affirmed 2025 outlook on the back of decent beer business and innovation. Nvidia extending pre-market gains, now rallying >+3% as the CEO said that demand for the Blackwell chip is “insane” which is lifting semiconductors. Amazon (AMZN -1.2%) plans to hire 250k seasonal workers across the U.S for the holiday season. The number is similar to last year’s holiday hiring signalling expectations for decent shopping ahead.

The VIX is testing 20 which acts has been resistance in the last two days. Cryptocurrencies mostly lower with Bitcoin trying to recover. Within the S&P 500, Energy leads the pack amid Middle East tensions. Oil rallying +5% after Biden’s comments. Brent futures testing 77 with short covering increasing. Financials slightly lower, KRE outpacing KBE both up. The US Dollar Index rising off session high near 101.8. Industrial metals lower; copper’s 20d ma moving higher. Precious metals positive with silver ahead of gold.

Tomorrow brings the much-anticipated BLS Employment Report including nonfarm payrolls which are expected to be rangebound at 140k. Fed’s Williams makes an appearance before the open.

Earnings

After-Market: AEHR, GRRR

Pre-Market: APOG

Sectors/Other Asset Classes:

- US 2yr +4bps to 3.69%, 5yr +5bps to 3.61%, 10yr +4bps to 3.83%, 30yr +2bps to 4.16%

- USD index: +$0.27 to $101.69

- Oil prices – ICE Brent: +4.8% to $77.46, WTI: +5.1% to $73.69, Nat Gas: +2.3% to $2.95

- Gold: +0.4% to $2,681.70, Silver: +1.6% to $32.43, Copper: -2.2% to $4.55

- Wheat: -0.7% to $6.15, Corn: -0.3% to $4.31, Soybeans: -0.1% to $10.55, Cotton: -1.2% to $0.73

- VIX: +1.70 to 20.60

- Bitcoin: -1.0% to ~60.2k

Central Banks/Inflation:

- ECB’s Schnabel signals shift on inflation, boosting rate-cut expectations (Reuters)

- BoE Governor Bailey says it could cut rates more aggressively on good inflation news (Guardian)

Economic Data:

- US:

- Weekly Jobless Claims Initial/Continuing 225k/1826k vs 220k/– cons, prior 219k/1827k

- Challenger Job Cuts Sept 72.821k, prior 75.891k

- S&P Global Services PMI Final Sept 55.2 vs 55.4 cons, prior 55.7

- ISM Services PMI Sept 54.9 vs 51.7 cons, prior 51.5

- Global

- Japan Jibun Bank Services PMI final Sept 53.1 vs 53.9 cons, prior 53.7

- EU Services PMI final Sept 51.4 vs 50.5 cons, prior 52.9

- EU PPI MoM Aug 0.6% vs 0.3% cons, prior 0.7%

{kind=link}

Discussion about this post