The FINANCIAL — The year 2014 set up the stage for new market dynamics that will influence consumer health in 2015.

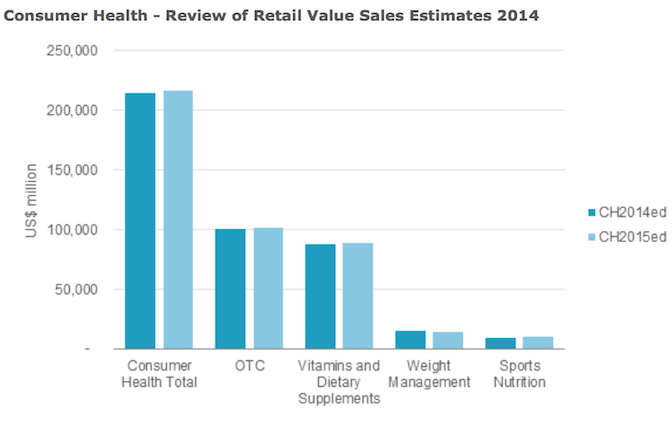

Our newest preliminary findings for the full year 2014 will be formally published on 19 January 2015. In the meantime, we provide a snapshot preview of how Euromonitor International compares its previous estimates with our most recent research. Overall, the industry grew at a healthy pace of 2.4% in constant terms in 2014 from 2013 (5.6% current/nominal terms) at fixed exchange rates. Surprisingly, this growth is more than one percentage point lower from our previous estimates. The year 2014 brought some growth difficulties in the United States, the largest consumer health market accounting for an estimated 28% of global retail value in 2013. A weaker than usual cold/flu and allergy seasons earlier in the year dampened the high prospects of sales. At the same time US consumers shied a bit away from their high consumption of vitamins and dietary supplements in favour of functional/fortified food and beverages, and fresh healthy foods in general. The new global estimates of growth seem a little bit lower due to a slowing down in the economies of Brazil, China and Russia, and also to the fact that the US$ dollar gained strength in the second half of 2014 – Euromonitor International typically reports figures in US$. This is not to say that consumer health is no longer a bright spot since the industry continues to grow at a healthy pace. Rather this is a wake-up call for the industry to work on priorities, focus on relevant therapies, manage competitive threats, and selectively invest in geographies that will lead to the next stage of growth.

{kind=link}

Discussion about this post