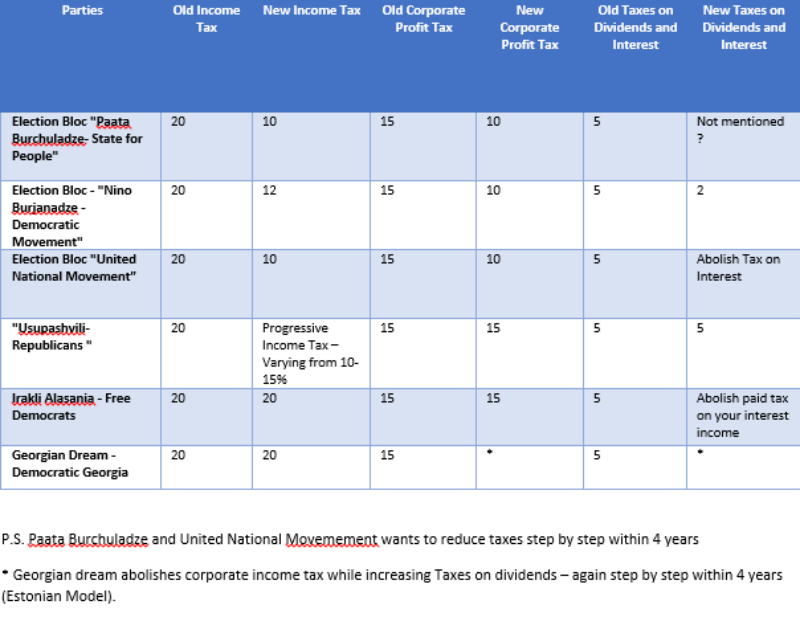

The FINANCIAL — Cutting taxes and achieving higher economic growth as a result is every politician’s dream. The 2016 parliamentary elections of Georgia showed just how important and controversial the question of taxation can become.

On the one hand, the Global Competitiveness Index Report that came out this month puts Georgia in the top 10 (9th place) among the countries with lowest tax rates. The current administration’s plans to abolish taxes on undistributed profit is likely to improve this ranking even more. On the other hand, many politicians argue that Georgian taxes are still “too high”, and some political parties have put deep tax cuts in the center of their economic platforms.

Are tax cut proponents right? Indeed, it may not be an easy question to answer.

One way to argue for tax cuts is to look at the relationship between the country’s tax rates and tax revenues over time. If tax rates are “too high” then a tax reduction should increase the tax revenues for the country (by giving businesses more incentives to operate, invest, or to come ‘out of the shadow’). If tax rates are already low and are not a binding constraint on business operations, then decreasing tax rates further will simply lower revenues. This kind of inverse U relationship between tax rates and tax revenues is know to economists as the “Laffer Curve”.

If we simply look at the relationship between tax rates and tax revenue in Georgia, it would appear that the country has been doing quite well after the tax reforms of 2005. In 2005, the government simultaneously reduced the number of taxes (from 22 to only 6) and lowered tax rates. They also managed to remove all unnecessary and inefficient interventions into private business and adopted simple and fair rules. The result of these reforms can be measured in the actual amount of tax revenue. Government managed to collect 1.19 billion lari in 2003 that amounted only 13.9 percent of GDP, while after tax reform both GDP and tax revenue increased dramatically and the equivalent figure for 2008 was 4.75 billion lari that is 24.9 percent of GDP.

However, it is interesting that the real GDP growth between 1996 and 2003 was actually higher (at 6.4%), than the real growth between 2004 and 2014 (5.5%). This correlation can give an idea that Georgia was better off economically during the years when the tax burden – a share of tax revenues in GDP – was at a low point, and therefore a further tax cut would benefit growth.

Yet, the problem of negative relationship between tax rates and growth in Georgia can be easily explained. In the early stages of development growth rates may be high (due to a very low base output base from which the country starts), while the tax burden may be low (due to low efficiency of tax collection). If the country reaches a higher level of GDP, while in the same time increasing the efficiency of tax collection, the growth rates will necessarily slow down while the tax burden will increase. This would give a misleading impression that the country’s economy is slowing down because of higher tax burden.

In this case it would be helpful to look at where the country’s tax burden stands in relation to other, similar countries.

Tax burden and incentives of economic agents in Georgia

How does the tax burden for Georgia compare to the similar measurement of the other transition economies? The Heritage Foundation computes tax burden as a share of GDP and Fiscal Freedom to evaluate the restrictive nature of the taxation system. According to the 2016 report, Georgia occupies 64th position among 186 countries in terms of the tax burden as a share of GDP. Georgia’s score of 24.8 is nearly an average score of the region (see the graph below).

Fiscal Freedom Index reveals the same pattern, since Georgia’s position in the list is 36, suggesting that there are only 35 countries out of 186 that has less restrictive taxation system than Georgia.

While it is obvious from the graph the Georgia does not have the lowest tax burden in the region, it is worth noting that three out of eight countries that score better in this regard are Azerbaijan, Kazakhstan and Turkmenistan. In these oil-driven economies GDP would be naturally much too high relative to the taxes government collects from non-oil businesses.

A more important issue to look at is whether tax rates constrain the decisions of household and businesses to work, consume and invest. If taxation system is restrictive for households and private business, tax cuts will stimulate them to increase consumption, work more hours, invest more money and expand their business.

The Global Competitiveness Report tracks down the effects of tax burden on the incentives to work and to invest. These indicators are computed based on the survey information, where respondents had to choose one number from 1 to 7 (1=to a great extent and 7=not at all) as an answer of a simple question: what extent do taxes reduce the incentive to invest (work)? According to the latest report, Georgia occupied the 11th (10th) position in the world and the first position in the region with a pretty high score 5.1 (5.2).

Furthermore, the survey asked the respondents to identify factors that are the most problematic for doing business. In Georgia businesses named inadequate educated workforce and access to financing as a top two problems, while tax rates and tax regulations came up in the ninth and tenth in this list – clearly taxes are not the binding constraint for growth of the Georgian businesses.

The verdict on tax cuts for Georgia

The idea of stimulating economic growth and creating new working places by reducing tax rates in Georgia needs further investigation. For now, it appears that tax burden is not a huge problem for Georgian businesses. Tax cuts may have a positive impact on economic growth, but they will not lead to the expected result without a new wave of reforms that give business a chance to fully embrace the new opportunities obtained from the tax reduction. For instance, such reforms may include helping small and micro businesses by liberalizing tax policy for them, developing capital markets that solve the problem of raising funds for business activities, improving antitrust law and breaking down barriers for motivated businessmen to enter new markets.

{kind=link}